ARE YOU EXPERIENCING BUSINESS INTERRUPTION CAUSED BY COVID-19?

THINGS YOU NEED TO KNOW IF YOUR BUSINESS IS INTERRUPTED

Business owners and operators are currently experiencing the pressure caused by COVID-19. If you find your business has been interrupted, now is the time to have a lawyer who specializes in COVID-19 Business Interruption insurance claims to review your coverage.

Have you or a loved one been involved in an accident? Speak to a lawyer for a free no obligation consultation

Or call us at (888) 699-7975

The global pandemic has currently displaced many workers across the world. As of April 3, 46 states are presently enforcing policies they have passed banning all nonessential businesses to remain closed during this pandemic. Other companies have begun taking more precautionary measures to reduce the spread of the Conornavirus.

Businesses are losing money daily that they are unable to operate. Owners and operators should be looking at their business interruption insurance for some relief during this time.

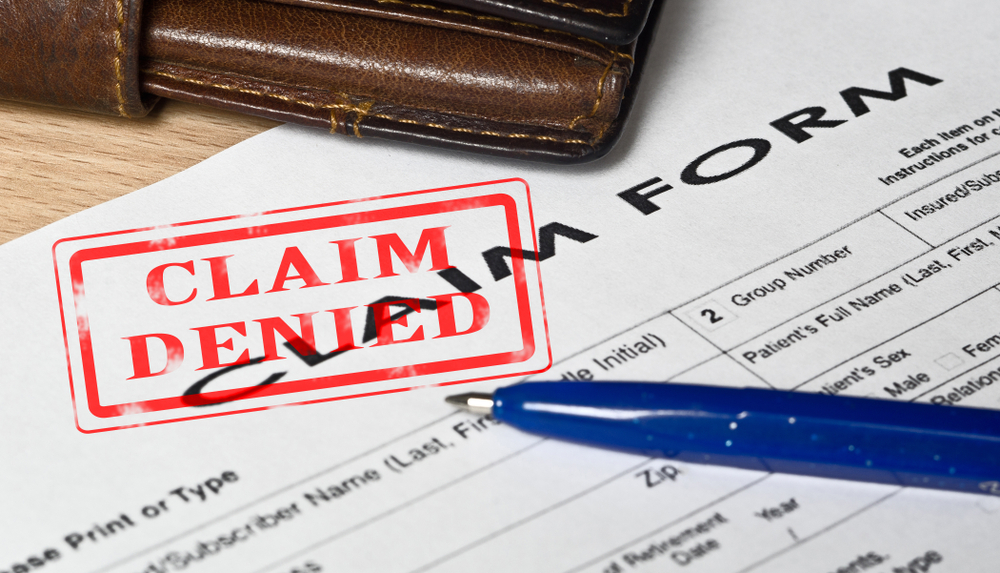

Unfortunately, many of these insurance companies are denying valid claims.

IS BUSINESS INTERRUPTION INSURANCE INSIDE YOUR POLICY?

Insurance policies can be challenging, understanding if you have not spent much time studying the language used to craft documents. A COVID-19 Business Interruption Insurance lawyer has spent unprecedented amounts of time examining these policies and its fine print. When you need guidance on filing your claim, make sure you reach out to these specialists.

WHAT IS BUSINESS INTERRUPTION INSURANCE?

Business interruption insurance is a type of policy that gets embedded into a different kind of policy. It is not a stand-alone policy you can add-on. When a situation forces your business to close, bills still have to be paid. Also known as business income insurance, this policy helps keep your business afloat in the event of an event beyond your control.

Business interruption insurance helps with:

- Recovering revenue lost due to business closure.

- Covering rent and other fixed utility costs during closure.

- If warranted, expenses to operate from a temporary location.

Each policy that contains business interruption insurance may cover additional costs or expenses that are associated with the revenue loss. Insurance providers that handle your business interruption policy will require you to show proof of the income lost. This will require you to prove to them what your business would have earned if the event had not occurred.

WHICH POLICIES HAVE BUSINESS INTERRUPTION COVERAGE?

Due to the fact that you cannot buy a stand-alone business interruption policy, it is important to know if your current policy includes it. You will find the information on your declarations page of your policy. The most common policy types that are inclusive of this coverage are listed below.

Commercial Property Insurance– You can add an endorsement or a rider to this type of policy to extend coverage to include business interruption losses. A rider is a provision or amendment to an insurance policy that extends or limits coverage.

Business Owners Policy– This insurance bundle is crafted for the smaller business owners. It consists of property, liability, and business interruption coverage.

Commercial Package Policy– Flexible coverage options that offer choices in coverage, including business interruption coverage.

Taking your declaration’s page to a skilled legal associate can help you determine which coverage you currently have. This may help you during the COVID-19 pandemic.

HOW ARE COMMUNICABLE DISEASES HANDLED BY A BUSINESS INTERRUPTION POLICY?

The likelihood of receiving a payout from your insurance policy willingly is probably next to none. The reason for this is after the SARS epidemic that took place between 2002 and 2003. Prior to SARS, the business interruption policies were worded in a way that communicable diseases could fit under the umbrella of coverage.

After the payouts that resulted in business interruptions during the SARS epidemic, many insurance companies made changes to their existing business interruption clauses. These changes excluded communicable diseases as a valid claim.

Legal Help with Insurance Declarations

Even if you cannot get a huge payout for business interruption purposes through the verbiage in your policy, that does not mean that you may have a total loss. Having a lawyer examine the terminology in your declaration’s page may uncover additional ways to recover losses during this time.

Even if your policy specifically limits the action you can take from the impact of the Coronavirus, and it may not be at a total loss for you. Contingent coverage, like ones that cover travel, could be the caveat you need to recover some of your income.

Having a lawyer who specializes in COVID-19 Business Interruption Insurance cases, may uncover exactly what you are missing. While it does not mean that your insurance company will not pay your claim, they will be more inclined to comply if you have legal representation.

WHAT TO DO IF YOUR CLAIM IS DENIED

TorkLaw offers a great resource as a reference when reading your declaration page. The firm breaks down the terminology you should look for when filing your claim. If you have been denied a claim, obtaining their legal expertise may turn the denial into an approval.

You may be entitled to a COVID-19 Business Interruption claim payout if you see the following terms within your policy:

- Business interruption or

disruption

- This coverage will pay out for lost profits during a disaster.

- Contingent business interruption

- When suffering losses from damage or losing access to suppliers of items critical to your business, the contingent plans cover those losses.

- Extra Expense Coverage

- The extra expense coverage pays out the extra expenses you may incur for normal business activities during an event. These include rent, utilities, etc.

- All Risk, Open Perils, and Special

Perils Coverage

- Pays for losses that stem from any cause that is not immediately excluded in the policy.

- Lost or Restricted Access Coverage

- Covers the losses that are incurred as a part of an order that restricts your access to your business. An example would be a shelter-in-place order.

- Civil Authority Coverage

- If the government orders closure of your business, this coverage pays for the losses attributed to it.

IF YOU FEEL YOUR CLAIM WAS INCORRECTLY DENIED

Your business is likely suffering from COVID-19 if you are looking into your business interruption insurance policy, don’t be alarmed if you don’t fully understand the technical terms. If you feel as though your claim was denied incorrectly, reach out to a TorkLaw specialist today to review your case.

At TorkLaw, we take the impact that COVID-19 has inflicted on the economy. We want to make sure that you and your business receive the compensation that you are entitled to.